First Home Buyers: $1,800 Monthly Repayment Reduction

Announcing the 'Help to Buy' scheme, the government is promising to offer reduced mortgage repayments and unlock promising long-term capital growth.

Launching in 2024, the new 'Help to Buy' scheme will enable first-home buyers to purchase with a 2% deposit.

The shared equity model sees the federal government co-purchase a 30 - 40% stake in the house.

And the home buyer takes out a loan for the remainder.

It is positioned differently from the current First Home Guarantee initiative, which enables a 5% deposit purchase without lenders' mortgage insurance, plus a loan for the balance.

Co-buying with the government for a smaller loan could trim monthly repayments by up to $1,829, according to research by Canstar.

However, the government's stake might limit capital growth upon sale, when the buyer will need to repay them with the proceeds.

The scheme could complicate moving up the property ladder in the future.

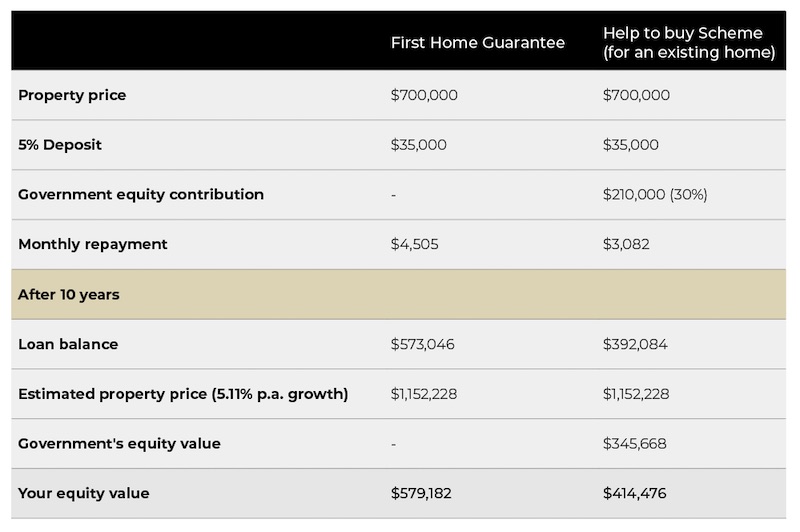

Comparison of First Home Buyer Government Schemes

First Home Guarantee (low deposit) vs Help to Buy (shared equity)

A decade later, the homeowner who partnered with the federal government would hold $592,294 in equity, in contrast to the potential $831,362 from an independent purchase.

In Brisbane, the limit is $700,000, so both 'Help To Buy' and First Home Guarantee repayment amounts would be $3,082 and $4,505.

Meanwhile, choosing the 'Help To Buy' scheme could mean monthly savings of $1,219 for a buyer in Perth.

First-home buyers looking to take advantage of the program should be aware of both the upsides and drawbacks of participating.

We'd suggest buyers reflect on what happens when they want to upgrade to a new home or sell. They will need to be aware the proceeds they would have had from an independent purchase will not be there.

Whilst this scheme will help buyers get into property today with lower repayments, they will have to share future capital growth with the government to repay them.

The government would also hold a greater stake in the property's equity compared to the buyer during the initial phase of the loan. This implies that in the event of a home sale, the government's share of the proceeds would surpass that of the homeowner.

In the initial phases of the loan, each repayment you make consists of a substantial interest component and a minor reduction in principal. As time goes on, the part dedicated to principal repayment grows while interest payments diminish.

Only upon reaching the full 30-year term would the equity distribution between the individual and the government become balanced. Before that point, the bank maintained a stake in 70% of the property.

The scheme's effectiveness hinges on first-home buyers refraining from purchasing houses beyond their affordable range. Some commentators cautioned that if the scheme prompted home buyers to stretch their budgets, it could perpetuate instability in the property market.

Research has shown that over the last 6 decades, any incentives or schemes that allow more expensive purchases tend to drive home prices higher.

In fact, since the launch of these schemes, the rate of homeownership has been declining.

Regardless of their original intention, these schemes often result in people buying homes that surpass their means.

While it's expected to help many first-home buyers, it will likely increase property prices that fit in that category. However, the consensus is that for three decades, governments on both sides have drastically unfunded what would help - social and affordable housing.

To learn more about 'Help to Buy' and other support for first-home buyers, speak to a Ramsey specialist Mortgage Consultant. We can review your situation and prepare a pre-approval based on your maximum borrowing power.

Book your appointment or call 1300 001 215